Published June 2026. This is Villa Andina's monthly cocoa market outlook: where prices are heading over the next one, three and six months, the supply and demand forces behind the move, and a data-led look at Peru's place in the global cacao trade. We publish it because we live in this market every day as an organic cacao producer and exporter from Peru, and we think buyers deserve the same picture we use ourselves.

New to the cocoa market? The world reference price is set by cocoa futures on the ICE exchange in New York (ticker CC=F), in US dollars per tonne. Nearly every contract for beans, nibs, paste, butter and powder prices off that benchmark, so when it moves, your cacao costs move with it. There is a short glossary at the end of this article.

1. The headline: a sharp rebound into a genuinely two-sided road

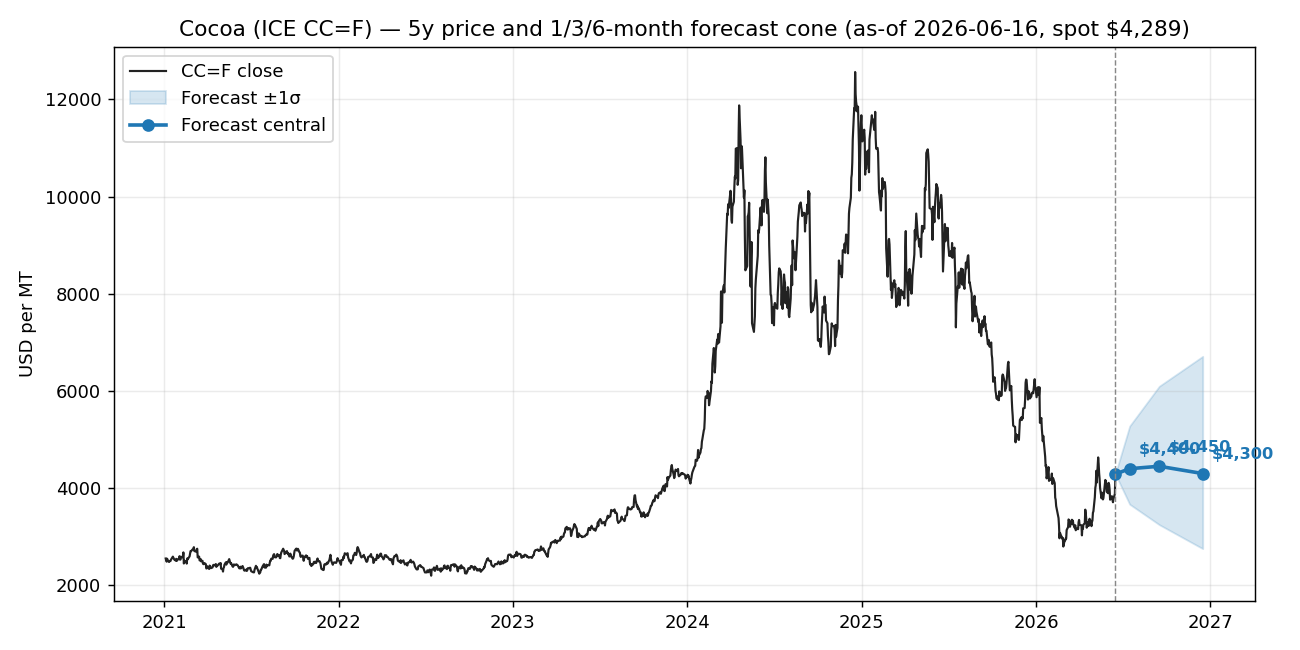

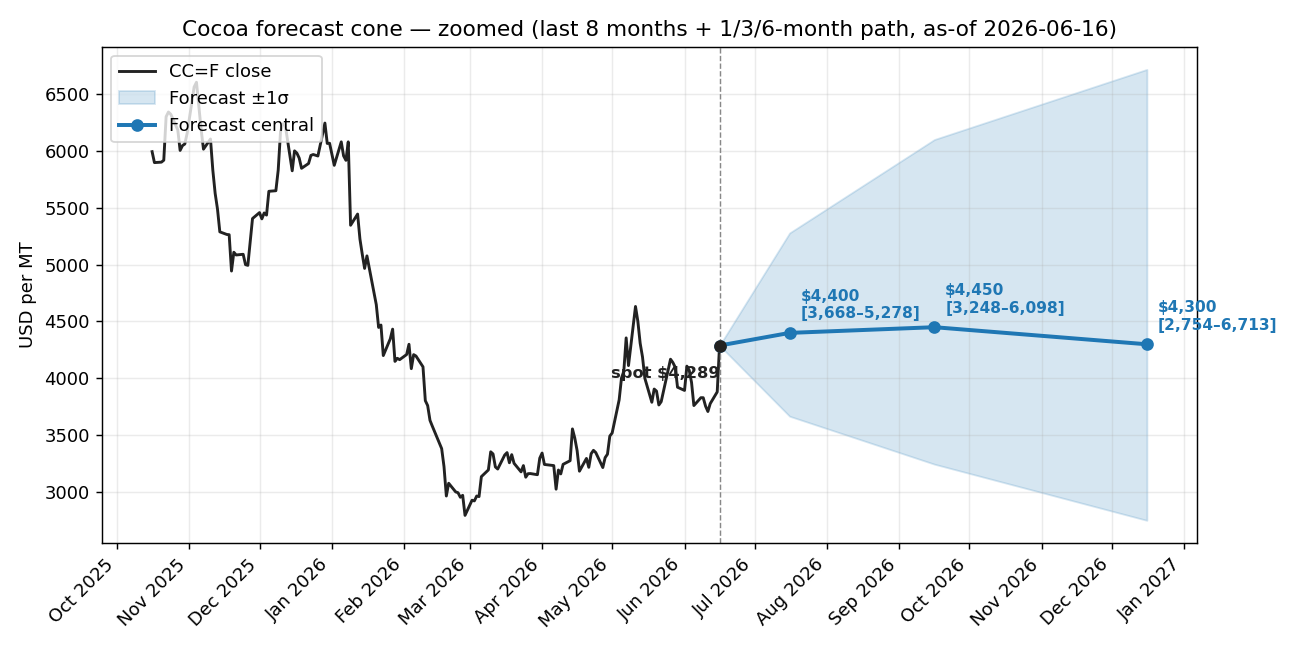

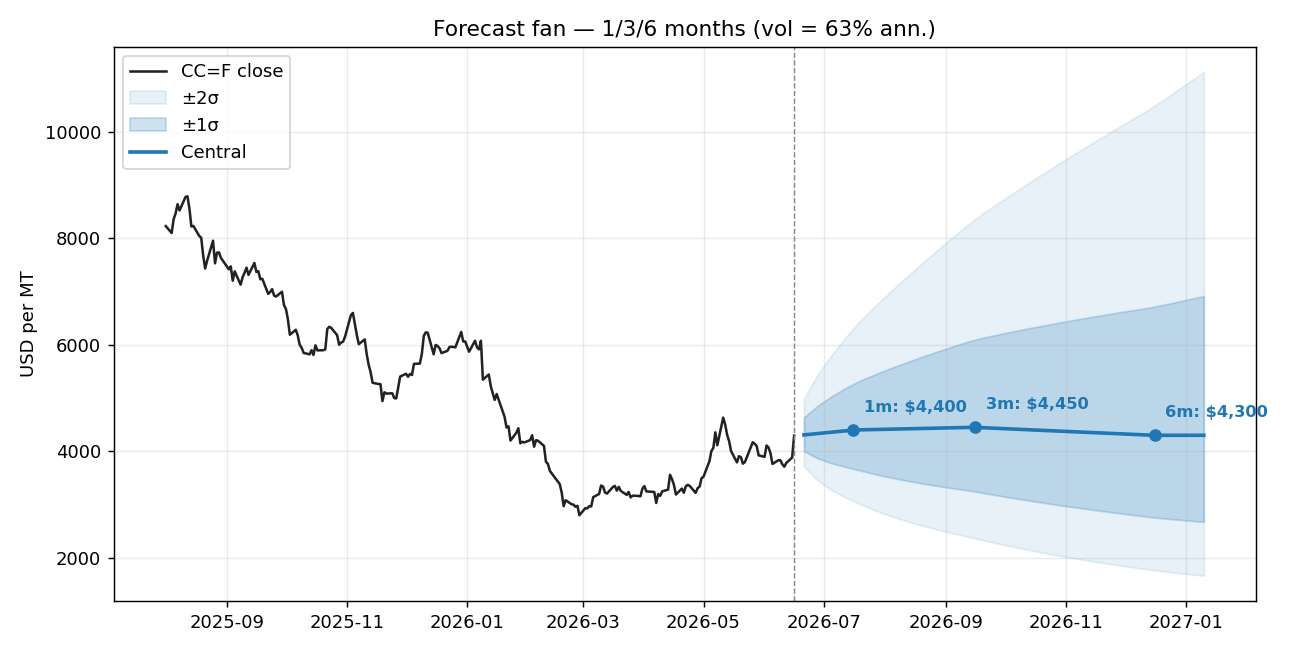

Cocoa futures closed around US$4,289 per tonne on 16 June 2026, up about 12% in a single week and 31% over three months. Yet prices are still roughly 57% below the record high near US$10,000 set in 2024. This is a recovery off a low, not a return to the peak.

Our view across the three horizons:

- One month (to mid-July): roughly US$4,300 to US$5,300, leaning firm. The rebound still has fuel from traders closing out bets that prices would fall, but the easy part of the move has happened.

- Three months (to mid-September): roughly US$3,250 to US$6,100, balanced. A wide range, because this is when the first hard reads on the next West African harvest arrive.

- Six months (to mid-December): genuinely two-sided, either near US$3,200 or near US$5,800. The big October main harvest in West Africa decides which. We would not bet on the middle.

The single most important idea in this report: the range is the message, not the central number. Cocoa is unusually two-sided right now, especially into year-end.

Zoomed in, so you can read the range at each horizon:

2. How cocoa got here: the 2024 super-spike, explained

To read 2026 you have to understand 2024. Cocoa spent a decade trading in a quiet band around US$2,000 to US$3,000 per tonne. Then, across 2023 and 2024, it went near vertical, briefly touching US$10,000. That is one of the largest moves any major agricultural commodity has ever made.

The cause was not speculation, it was three consecutive deficit seasons in West Africa, which grows roughly 70% of the world's cocoa. Côte d'Ivoire and Ghana alone are about 60% of global supply, and both were hit at once by a stack of problems: heavy early rains followed by hot, dry Harmattan conditions; outbreaks of black pod and cocoa swollen shoot virus, a disease with no cure that forces farmers to cut down trees; ageing tree stock past its productive prime; illegal gold mining swallowing farmland in Ghana; and years of farmgate prices too low to justify replanting. Supply simply could not keep up, global stocks drained, and the price did the rationing.

The retrace since the 2024 peak is the second half of that story. Very high prices did two things: they pulled some new supply and a lot of selling forward, and they began to destroy demand. That brings us to today's tug-of-war.

3. What is moving the market now

Supply: the bull case, but it is about the next crop

Most of the upside story is about a harvest that has not happened yet. Early surveys of the 2026/27 West African trees show below-average cherelle set. Cherelles are the small early pods that grow into the main October harvest, so a weak cherelle count is an early warning on supply. Soil moisture across the cocoa belt is also running dry, and forecasters say an El Niño weather pattern, which tends to bring hotter and drier conditions to West Africa, has formed.

We track our own in-house climate signals (rainfall, soil moisture, vegetation health and ocean indices). As of mid-June they read closer to neutral than to a confirmed El Niño, so we treat West African weather as a building risk into October, not a confirmed shortfall. It is the single most important thing to watch this quarter, because the structural problems behind the 2024 spike (ageing trees, disease, under-investment) have not gone away. They set a high floor under supply risk.

Demand: the quiet bear case

Pulling the other way is demand. Grindings, the volume of beans processed into liquor, butter and powder and the best read on real consumption, are running down about 2% year on year. Two years of record prices pushed manufacturers to reformulate, shrink bar sizes and lean on substitutes, with Europe (the largest grinding region) feeling it most. The 2024/25 season actually recorded a small global surplus of beans. That demand softness caps how far prices can run unless the next harvest genuinely disappoints.

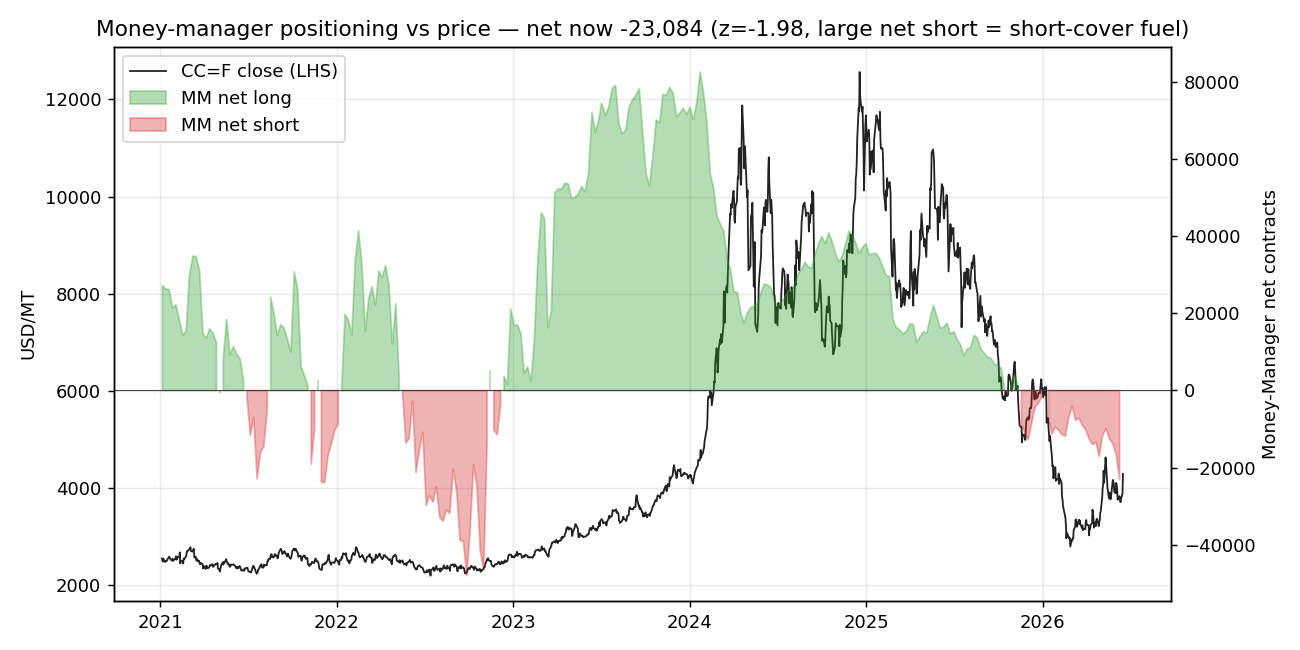

Positioning: why a 12% week happened

For the more technical reader, futures positioning explains the timing of this month's jump. Going into June, speculative money managers held a large net short, a big collective bet that prices would keep falling. A heavy short base is exactly the fuel that produces sharp rallies: when the news turns even slightly bullish, those traders have to buy back their positions, and that buying feeds on itself. That is short-covering, and it is a large part of the 12% move. The positioning charts are in the technical appendix.

4. Peru in focus: the data behind a rising origin

This is the part you will not easily find elsewhere. Using Peruvian customs records, here is what Peru's cacao trade actually looks like, and why it matters for buyers.

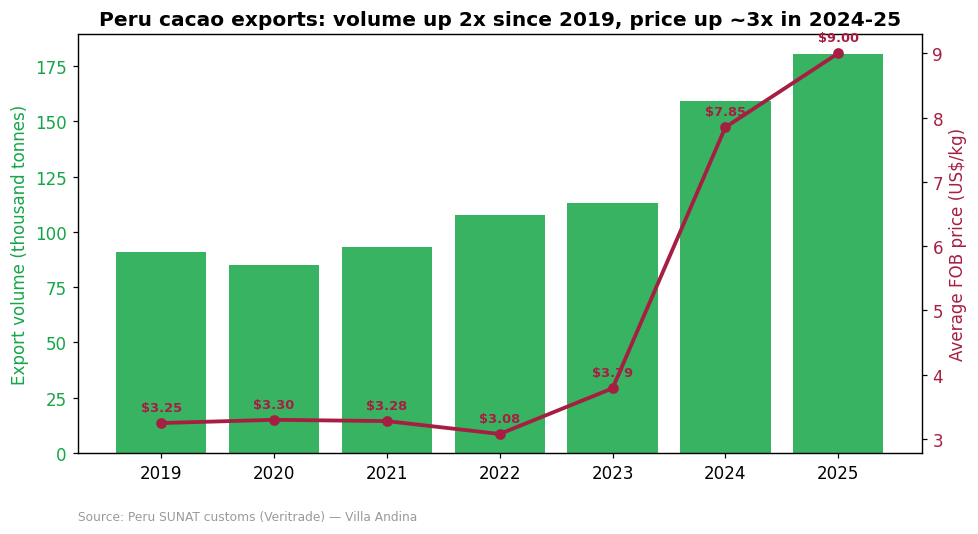

Volumes doubled, prices roughly tripled

Peru's cacao exports grew from about 91,000 tonnes in 2019 to roughly 180,000 tonnes in 2025, nearly doubling in six years. The average export price (FOB) tracked the global spike, climbing from around US$3.3/kg in 2019 to 2022 up to US$7.85/kg in 2024 and US$9.0/kg in 2025.

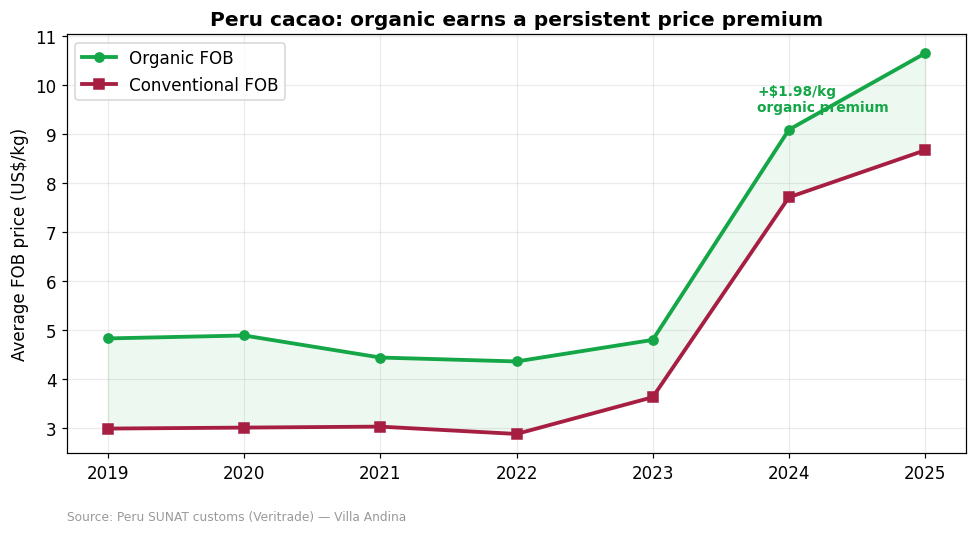

Organic earns a real, persistent premium

Organic cacao is not just a label in Peru, it is a price. In every year since 2019, organic export FOB has sat clearly above conventional, and in 2025 organic averaged US$10.64/kg versus US$8.66/kg for conventional, a premium of nearly US$2.00/kg (about 23%). Just as telling, organic volume nearly doubled in a single year, from about 17,000 tonnes in 2024 to 31,000 tonnes in 2025, so the premium is being earned on a fast-growing base, not a niche. For buyers building certified or clean-label programs, this is the structural reason Peru is worth a look.

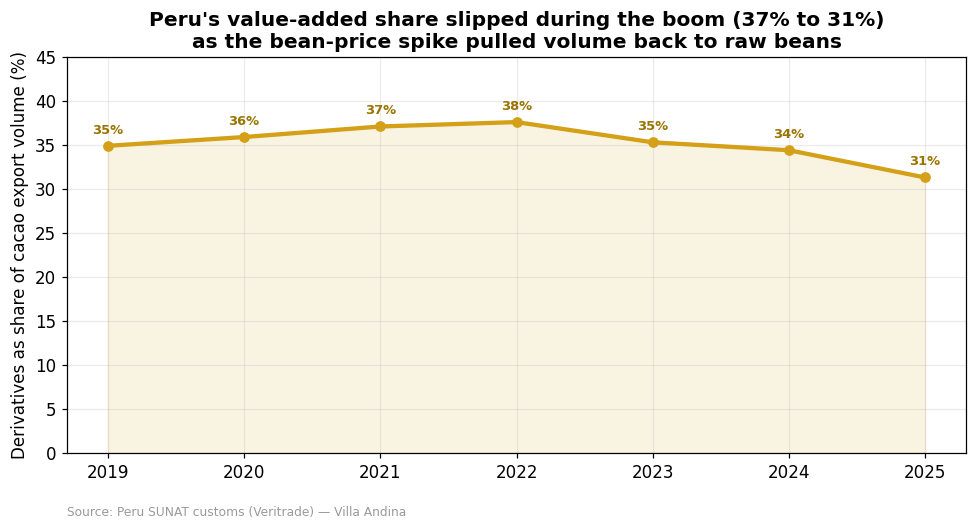

The value-added paradox

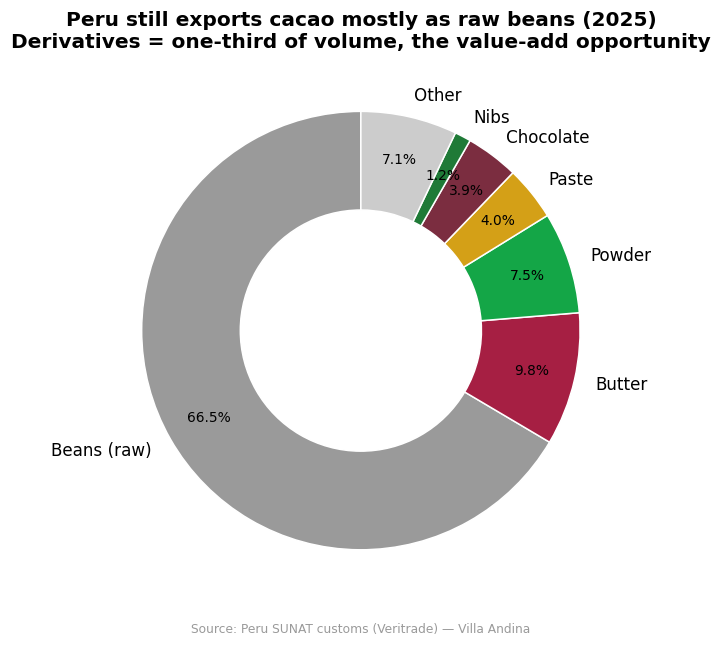

Here is a counterintuitive finding. You might expect a price boom to push an origin up the value chain, into nibs, paste, butter and powder. Peru did the opposite. The derivatives share of export volume actually fell from about 37% in 2021 to 31% in 2025, because the spike in raw bean prices made simply shipping beans the most profitable, lowest-effort option. As bean prices normalize from the 2024 extreme, that logic reverses: value-added products become relatively more attractive again, and the under-built derivative capacity becomes the opportunity. This is precisely where Villa Andina focuses, organic nibs, paste, butter and powder rather than commodity beans.

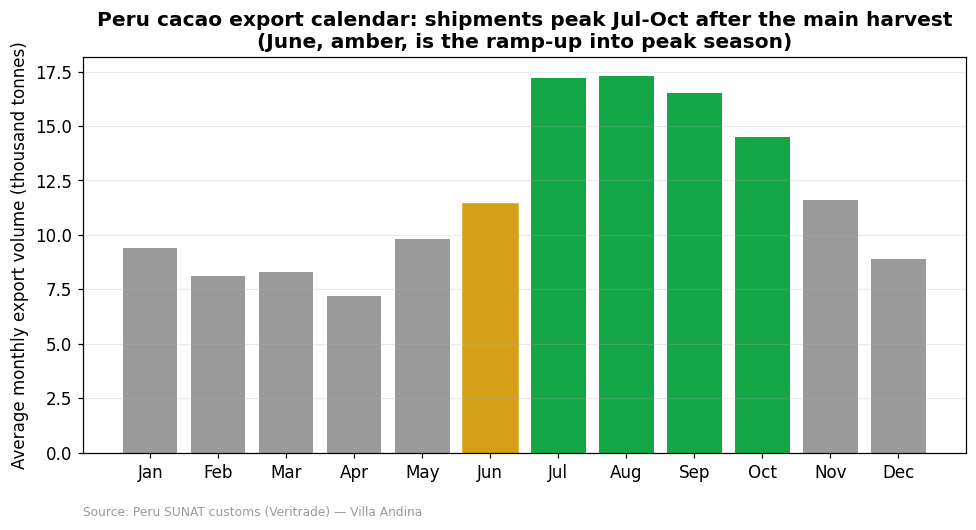

The export calendar, and why timing matters now

Peru's cacao ships on a clear seasonal rhythm. Averaged over recent years, export volumes are lowest in the first and second quarters and peak from July through October, following the main harvest, with June the ramp-up month into that peak. For a buyer, that means fresh-crop availability and quality are best, and lead times shortest, in the middle of the year, which is exactly where we are now.

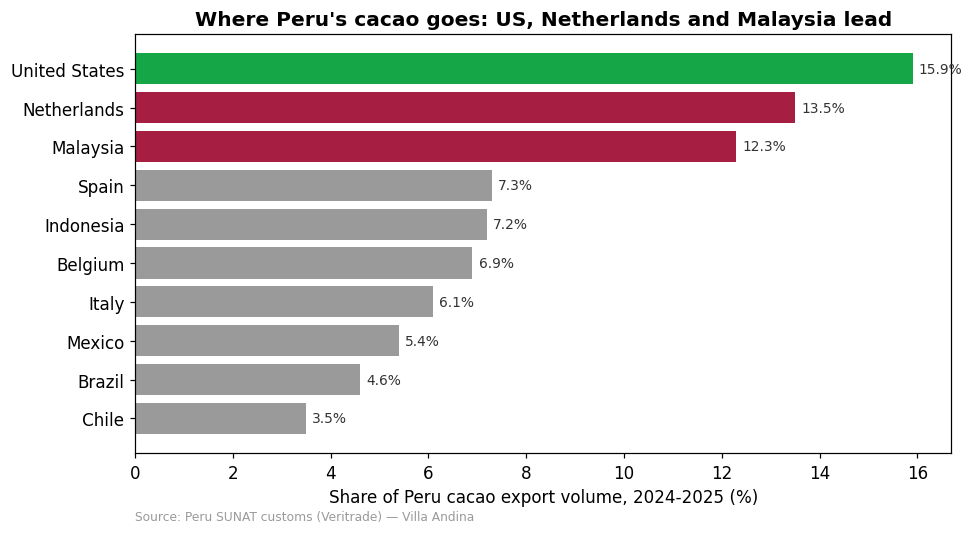

Where it goes, and in what form

Peru's cacao is diversified across continents. Over 2024 and 2025 the United States (about 16%), the Netherlands (13%) and Malaysia (12%) were the three largest destinations, with strong demand also from Spain, Indonesia, Belgium and Italy. Europe and Asia together take the majority, which matters for freight planning, certification and (for powder bound for the EU) cadmium compliance.

And by product, about two-thirds of Peru's 2025 cacao volume still left as raw beans, with butter, powder, paste, chocolate and nibs making up the rest. That one-third is the value-add frontier.

5. What this means for cacao buyers

Putting the global view and the Peru data together, three practical takeaways:

- Cover part, stay flexible. Near-term offers are firm and the supply risk into October is real, but the six-month range is genuinely two-sided. Securing part of your Q3 coverage while leaving room to react into year-end is a sensible way to handle that.

- The timing window favours buyers now. We are at the peak of the Peruvian harvest, so fresh-crop quality is at its best and lead times are short. With near-term prices leaning firm, this is a reasonable moment to lock in part of your needs rather than wait for a picture that could break either way.

- Organic and value-added are where Peru's edge is. The organic premium is durable and the derivative segment is under-built, so for certified, clean-label or value-added cacao programs, Peru is a strong, traceable origin. On EU-bound cacao powder, note that Peruvian origin tends to run low on cadmium relative to the EU limit that applies to powder and chocolate.

We are an organic superfoods producer and exporter from Peru, working directly with farming communities. You can explore our organic cacao, our wider superfoods range, and our full product list, all fully traceable.

Frequently asked questions

Why did cocoa prices spike in 2024? Three consecutive deficit harvests in West Africa, which supplies about 70% of the world's cocoa, driven by adverse weather, disease (black pod and swollen shoot virus), ageing trees and chronic under-investment. Supply could not meet demand, stocks drained, and the price rose to ration the shortage, briefly reaching US$10,000 per tonne.

Will cocoa prices come down in 2026? They already have, to about US$4,300 in mid-June 2026, roughly 57% below the 2024 peak. Our forecast sees a firm near term and a genuinely two-sided six-month outlook: either back toward US$3,200 if the October West African harvest is normal, or up toward US$5,800 if it disappoints. The range matters more than any single number.

What is driving cocoa prices in 2026? A tug-of-war. On the bullish side, weak early signals for the next West African crop, dry soils and El Niño risk. On the bearish side, demand down about 2% as high prices destroy consumption, and a recent global surplus. Futures positioning amplifies the swings.

Is organic cacao more expensive than conventional? Yes. In Peru, organic cacao has earned a persistent FOB premium, nearly US$2.00 per kilo (about 23%) in 2025, and organic export volume is growing quickly.

When is the Peruvian cacao harvest? Peru harvests cacao across the year with a main crop mid-year. Exports peak from July to October, so fresh-crop availability and quality are best in the middle of the year.

Key terms

ICE CC=F. The New York cocoa futures contract, the global reference price in US$/tonne.

Grindings. The amount of cocoa processed into liquor, butter and powder. The best proxy for real demand.

Main crop and mid-crop. West Africa's two harvests. The larger main crop runs roughly October to March; the smaller mid-crop April to September.

Cherelle. A young cocoa pod. Early cherelle counts foreshadow the size of the coming harvest.

FOB. Free On Board, the price of goods loaded at the export port, before freight and insurance.

Deficit and surplus. Whether world production falls short of or exceeds grindings in a season. Deficits drain stocks and lift prices.

Technical appendix: for the trading desk

Method. Spot anchor ICE CC=F US$4,289/MT (16 June), +12.0% week on week, +31.6% over three months. Realised 90-day volatility is about 63% annualised. The forecast ranges are the spot price multiplied by exp(±sigma), with sigma scaled by the square root of time (about 18% at one month, 32% at three months, 45% at six months), so the bands widen with the horizon.

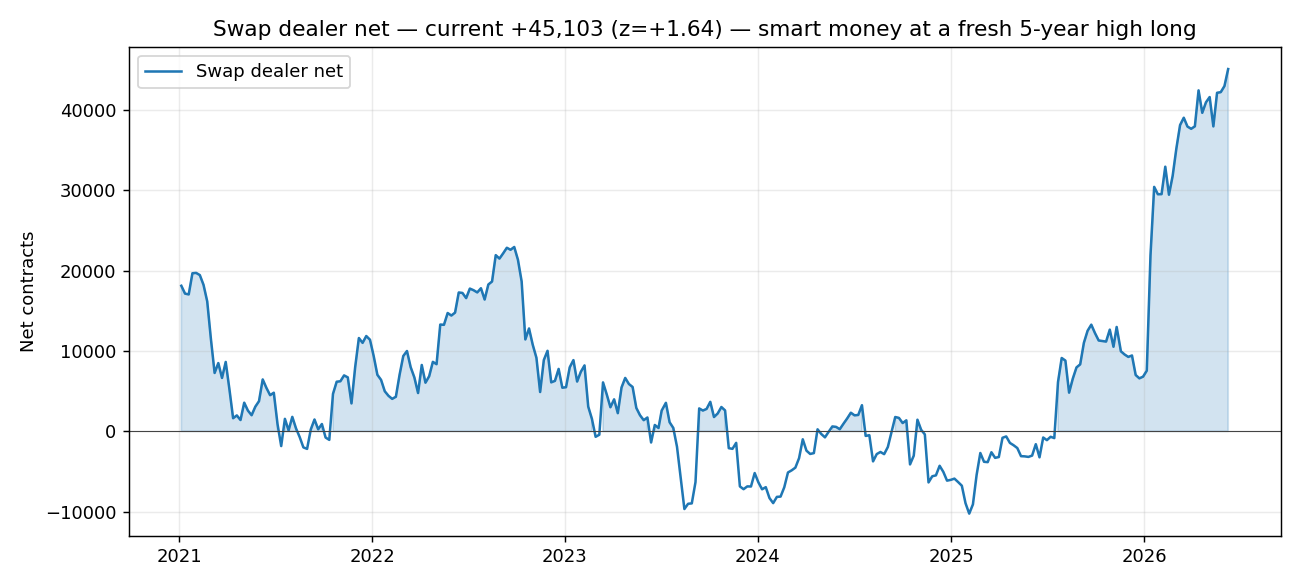

Positioning. Money managers are net short roughly 23,000 contracts, about two standard deviations below their one-year norm, which is contrarian-bullish fuel for further short-covering. Swap dealers are net long around 45,000 contracts, a fresh five-year high, and have added through the rally rather than selling into it. Against that, the realised balance is soft (a small 2024/25 surplus, grindings down about 2%), and macro cost pressure has eased, with Brent crude back near US$97 from March's US$126 spike.

On the model. We also run a machine-learning model (gradient-boosted trees) on a monthly panel of price, positioning, weather and macro features. It does not reliably beat a simple random walk out of sample at the three-month horizon, which is normal for commodity prices, so we use it for its uncertainty band and its driver attribution (it independently flags weather and positioning as the dominant forces), not for a single point forecast. Methodology and sources available on request.

This article is a market read for general information, not investment advice. Prices move daily; all figures are as of 16 June 2026. Global price, positioning and balance data are sourced from ICE, the CFTC and the ICCO; Peru export statistics are from SUNAT customs records via Veritrade.